How can we forget this iconic scene from this iconic movie?

Many moneylenders often come across situations where borrowers clearly postpone or refuse to pay back the loan they have taken from their moneylenders.

That’s when the borrowed asset (money, here) is termed a Non-Performing Asset (NPA).

This means that the asset no longer generates income for the lender because the borrower is not repaying the principal amount and the interest.

To get a broader view of how these non-performing assets work, read our blog to understand NPA Meaning in Banking, the Types of Non Performing Assets, the Impact of NPA, and the Difference between Gross NPA and Net NPA.

Content:

- NPA Meaning in Banking

- Non Performing Assets Example

- Types of Non Performing Assets

- Impact of NPA

- Difference between Gross NPA and Net NPA

- Quick Summary

- FAQs

NPA Meaning in Banking

Any financial security owned by a bank is considered an asset. The interest we pay on loans is the primary source of income for banks; hence these loans are classified as assets.

So, when borrowers cannot repay the amount, these assets are coined as “Non Performing Assets” because they are not generating any income for the bank.

The bank gives the borrower 90 days to repay the loan. If the repayment is not done within that time frame, the assets are declared as non-performing.

Non Performing Assets Example

Assume that ‘A’ has obtained a loan from the bank for ₹1,00,000 with a one-year maturity period. It’s been 90 days now that he hasn’t paid the interest nor the principal amount after the maturity period. This amount that the bank has failed to collect from its borrower is termed a non-performing asset.

Ideally, non-performing assets are listed on the balance sheet of a bank or any other financial institution.

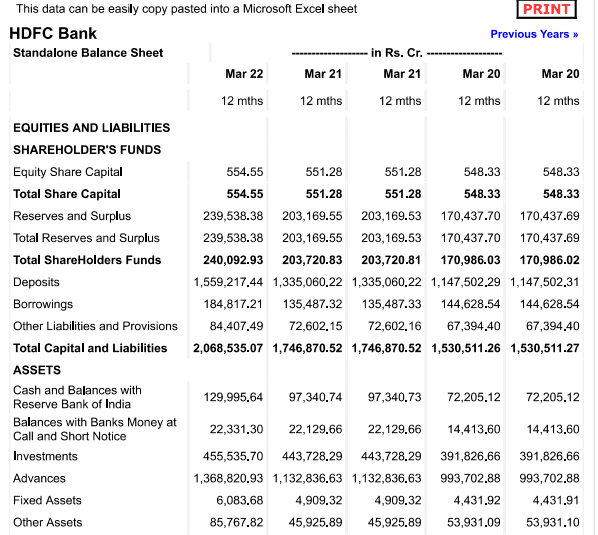

Let me present to you the Standalone Balance Sheet of HDFC Bank.

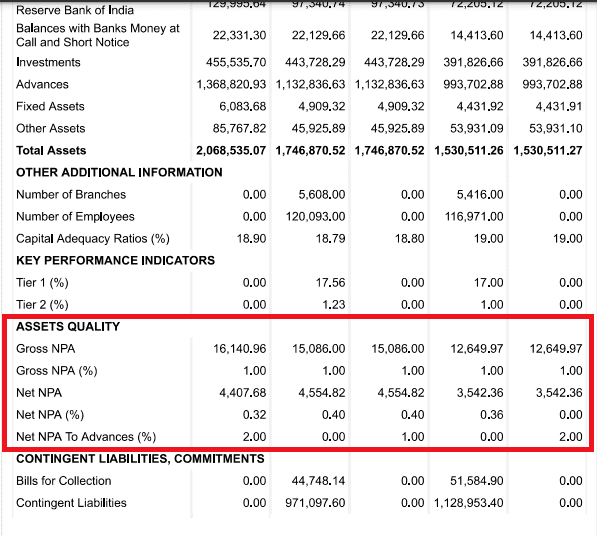

In the image, you can see the ‘Assets Quality’ section, where you can find the Gross NPA and Net NPA categories. The value (in crore) depicts the cost of assets that are not generating any income.

It’s not wise for the companies to have high NPAs, because these assets are non-performing in nature.

Types of Non-Performing Assets

The three types of Non-Performing Assets are:

- Substandard Assets

- Doubtful Assets

- Loss Assets

- Substandard Assets

These are assets that are not performing for a period less than or equal to 12 months.

- Doubtful Assets

These are assets that are not performing for a period of 12 months or more.

- Loss Assets

These assets are regarded as ‘uncollectible,’ as they have very little or no monetary value. Although they might have some recovery value, they are no longer considered assets of the bank.

Now that we know what is non-performing assets, NPA Meaning in Banking, and the types of non-performing assets, let’s learn what is the impact of NPA.

Impact of NPA

Let me explain the impact of NPA to you from two different perspectives.

- From the shoes of the banks –

Due to higher NPA rates, banks will suffer significant revenue losses that will potentially affect their brand image.

Also, due to insufficient funds, banks will have to increase the interest rates on loans to maintain their profit margin.

- From the shoes of the borrowers –

Banks will be suspicious in sanctioning loans to a borrower whose accounts are already under NPA.

It will greatly have a negative impact on the brand image of the borrowers.

Difference between Gross NPA and Net NPA

It is mandatory for banks to display their NPAs on their balance sheet. It is provided in two categories.

As shown in the image above (the HDFC bank’s standalone balance sheet), the ‘Assets Quality’ section represents two rows: Gross NPA and Net NPA.

These two metrices represent the value of the non-performing assets in a bank.

Gross NPA (GNPA) denotes the total of all the loan assets that haven’t been repaid by the borrowers within the ninety-day period.

Whereas,

Net NPA (NNPA) is the amount remaining after deducting doubtful and unpaid debts from the GNPA. It is the actual loss suffered by the bank.

For a better understanding, refer to this table-

| Gross NPA (GNPA) | Net NPA (NNPA) |

| Gross NPA (GNPA) denotes the total of all the loan assets that haven’t been repaid by the borrowers within the ninety-day period. | Net NPA (NNPA) is the amount remaining after deducting doubtful and unpaid debts from the GNPA. It is the actual loss suffered by the bank. |

| (Substandard + Doubtful + Loss) assets | Net NPAs = Gross NPAs – Provisions |

| It does not qualify the organization’s actual loss. | It qualifies the organization’s actual loss. |

| The bank provides a time limit after which the principal and interest must be repaid. After this period expires, the asset becomes non-performing. | There is no such time limit in Net NPA. |

Quick Summary

- Non Performing Assets are loans that are not repaid to the borrowers within a stipulated period of time. They no longer serve as an asset as they don’t generate any income for the lenders.

- The three types of Non Performing Assets are:

- Substandard Assets

- Doubtful Assets

- Loss Assets

- The impact of NPA is categorized in two different perspectives: Banks and Borrowers.

- There are two types of NPA: GNPA and NNPA

- Gross NPA (GNPA) denotes the total of all the loan assets that haven’t been repaid by the borrowers within the ninety-day period.

- Net NPA (NNPA) is the amount remaining after deducting doubtful and unpaid debts from the GNPA. It is the actual loss suffered by the bank.

FAQs

1. What is the current NPA in India?

NPAs of the banking sector dropped below 6% as of March 2022. According to RBI, Bank NPAs may go beyond 8% by September 2022.

2. What are NPA Ratios?

NPA Ratio gives us an idea of how much of total advances are not recoverable.

Provision Coverage Ratio = Total provisions / Gross NPAs.

3. How is NPA calculated?

NPA is calculated by dividing the non-performing assets by total loans will give the NPA ratio in decimal form. Then, multiply it by 100 to get the NPA percentage.

Suppose the total amount of loan provided by a bank is ₹20,00,000.

NPA= ₹1,00,000

Therefore the NPA ratios is 1,00,000/20,00,000 = 0.05

NPA percentage = 0.05X100 = 5%.

Click the link to access the web story now: What is NPA